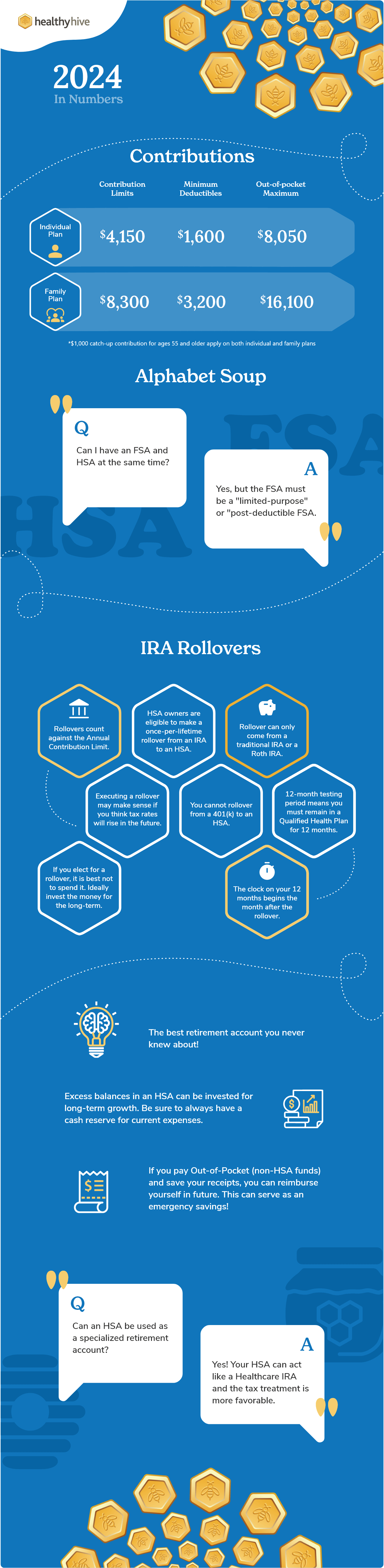

All about HSAs

If you receive health insurance through your employer you may have heard of a health savings account (HSA). HSAs are financial accounts, not insurance products. Participants enrolled in a qualified High Deductible Health Plan (qHDHP) can open and contribute to an HSA. Employers may provide matching contributions to build employee incentives.

Alphabet Soup

Don’t let the confusing employee benefit alphabet soup overwhelm you, particularly as it relates to your HSA. An HSA is very different from a flexible spending account, or FSA. FSA balances need to be spent by the end of the year. Money not spent in time from an FSA is lost. Health savings account balances roll over to the next year and if you quit your job you can take the funds with you (portability). HealthyHive’s annual HSA infographic below hopefully helps reduce the alphabet soup confusion.

Stealth Retirement Accounts

Health savings account balances can also double as a long-term retirement account. Specifically, you can invest funds in an HSA. Think of an HSA as a specialized IRA (individual retirement account) that can fund healthcare spending now or in retirement. JP Morgan estimates that 14% of total retiree spending (over age 75) is healthcare-related. Indeed, for the 75+ age cohort, healthcare is the second highest spending category after Housing.

Tax Unicorn

Triple tax-advantaged gifts from the IRS are rarer than unicorns. HSAs are the only retirement savings account we know of that carry a triple tax advantage.

Payroll contributions to an HSA avoid FICA taxes, unlike in a 401(k). That alone comprises a 7.65% relative value gain on Day 1 of any contribution. Second, earnings in an HSA are not taxed. This is like conventional IRAs or employer-sponsored retirement plans like a 401(k) or 403(b). Finally, withdrawals are never taxed provided the funds are spent on qualified healthcare expenses.

In short, excess HSA balances may be an ideal investment opportunity if you have a long time horizon and no immediate plans for expensive medical services. Investing obviously involves risk so we encourage HSA owners to retain at least one year of estimated out-of-pocket spending in cash.

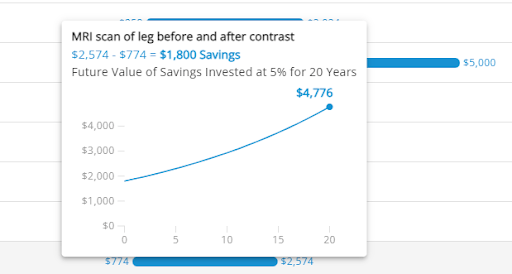

Price Transparency Education

The connection between healthcare price transparency and retirement planning may not be intuitive, but it is real. When HSA owners begin to understand the retirement angle & tax advantages of their account, they are more motivated to avoid wasteful spending. The plot below illustrates the power of healthcare price comparisons for HSA owners. Suppose a savings of $1,800 (for a leg MRI in this example) is invested for 20 years. If the investment rate of return averages 5% over this period it would grow to $4,776. Taking time to call a few doctor offices for price comparisons can yield significant benefits over the long-term.

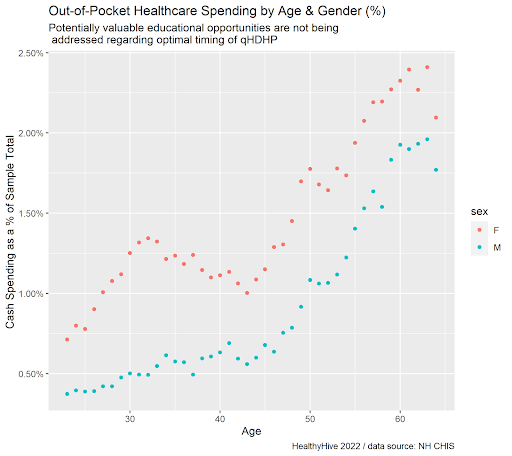

Females and HSAs

We have spent a lot of time analyzing medical claims data. Some of our insights have been quite eye opening. Females account for a larger proportion of total healthcare spending than males. This is not particularly shocking given females give birth to offspring and the US healthcare system takes full advantage of this fact.

We decided to sample our claims data library to examine the out-of-pocket exposure between the sexes. Instead of looking at total expenditures by age and gender we isolated the deductibles, co-pays, and coinsurance amounts for each claim. These three amounts comprise the majority of cash payments during healthcare interactions in the US. As data nerds, we feel the insights were meaningful and important, particularly for females!

Female HSA owners between the ages of 25 and 42 should pay particular attention to price transparency. While the relative out-of-pocket exposure between the sexes is consistent across the age spectrum, the gap is widest between 25 & 42. The gap peaks around ages 33 or 34.

In many cases females may only have access to high deductible health plans through their employer. However, when faced with the option between a higher premium plan (lower deductible) and a higher deductible plan (lower premium), females in the family formation stage of their lives may be better off to avoid HSA-eligible plans. Once family formation years have passed females can move back to a high deductible plan and continue funding the HSA.

If a high deductible plan is the only option it means comparing prices can yield the most value for the 25-42 female age cohort. Avoiding hospital settings for routine healthcare visits and services is possibly the most powerful rule of thumb for anyone looking to reduce out-of-pocket spending. Again, this is particularly the case for females.

Becoming a more engaged healthcare consumer requires effort and discipline. But if you own an HSA and appreciate the fact that paying too much on routine healthcare services could delay your retirement plans, an assertive and inquisitive demeanor can go a long way.

About HealthyHive

Our mission is to help retirement advisors & employees make the health + wealth linkage through our HSA education services. We deliver our education curriculum through advisors and directly to companies. Please contact chall@hiveaway.com to learn more.

For Individuals

Willow Talk

About Us